How to Create a Budget That Actually Works in 2026

You’ve tried budgeting before. You downloaded the app, created the spreadsheet, and felt motivated for exactly three days. Then life happened—an unexpected car repair, a friend’s birthday dinner, or just general exhaustion from tracking every penny. The budget app gathered digital dust, and you went back to hoping there’s enough money in your account.

Sound familiar? You’re not alone. While financial experts recommend budgeting as the foundation of financial health, only 32% of households actually maintain a detailed budget. The problem isn’t that budgeting doesn’t work—it’s that most budgeting advice sets you up for failure.

This guide shows you how to create a budget that actually works for real life. Not a restrictive spending diet you’ll abandon next month, but a sustainable system that helps you control your money without controlling your life. You’ll learn the 50/30/20 framework (plus better alternatives), how to handle irregular income, and most importantly—how to stick with it.

Let’s build a budget you’ll actually use.

Why Most Budgets Fail (And How to Avoid It)

Before we build your budget, let’s understand why previous attempts probably failed:

Too restrictive:

Cutting out all “fun” spending creates the financial equivalent of a crash diet. You feel deprived, then binge spend.

Too complicated:

Tracking 47 different spending categories or logging every £2 coffee purchase isn’t sustainable. If it takes more than 10 minutes per week, you won’t maintain it.

Unrealistic goals:

“I’ll save 50% of my income!” sounds great until you realize your actual expenses make that impossible. Then you feel like a failure and quit.

No flexibility:

Life is unpredictable. Budgets that can’t handle unexpected expenses or irregular income are doomed from the start.

Wrong method:

The popular 50/30/20 rule doesn’t work for everyone, especially those with high housing costs or student loans.

The solution? A budget that’s simple, realistic, and built around your actual life—not an idealized version of it.

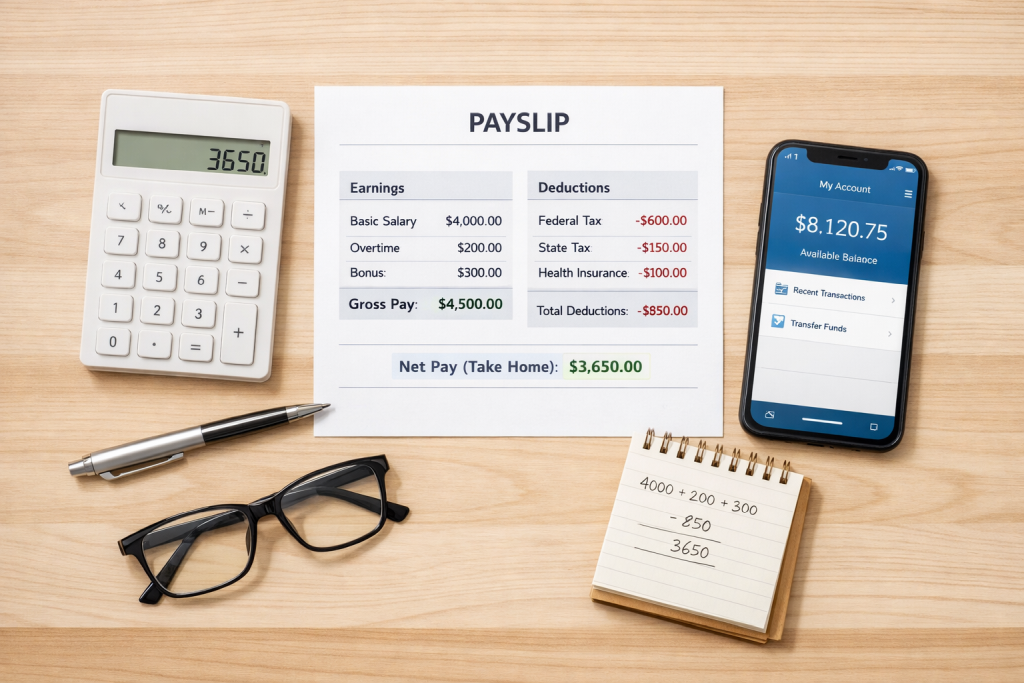

Step 1: Calculate Your After-Tax Income

Start with what you actually receive, not what you earn. Your budget should be based on take-home pay, not gross salary.

For salaried employees:

Check your recent payslip. Your take-home pay (after tax, National Insurance, and pension) is your budget starting point. Multiply by 12 and divide by 12 to get your true monthly average if you’re paid weekly or fortnightly.

For variable income:

Take your last 6 months of income, add it together, divide by 6. Use this conservative average. Better to underestimate than overestimate.

For freelancers/self-employed:

Use last year’s net profit divided by 12. Set aside 25-30% immediately for taxes before budgeting.

Multiple income sources: Add all regular income together. Include only consistent side income you can count on monthly.

Example: Sarah earns £2,800 gross monthly but takes home £2,240 after tax and pension. She also freelances, averaging £400/month after tax. Her budget income: £2,640/month.

Step 2: Track Your Current Spending (Just for 30 Days)

You can’t create a realistic budget without knowing where your money actually goes. But don’t panic—you only need to do this intensive tracking once.

The simplest method:

Download your bank statements for the past 2-3 months

Categorise every transaction into:

Housing, Transport, Food, Utilities, Debt, Insurance, and Other

Calculate monthly averages for each category:

Be honest—include that daily coffee, streaming services, and impulse Amazon purchases

Use a simple spreadsheet or even pen and paper. Fancy apps aren’t necessary—clarity is.

Reality check: Most people underestimate spending by 20-30%. That’s why this step is crucial. You might discover you’re spending £200/month on takeaways when you thought it was £80

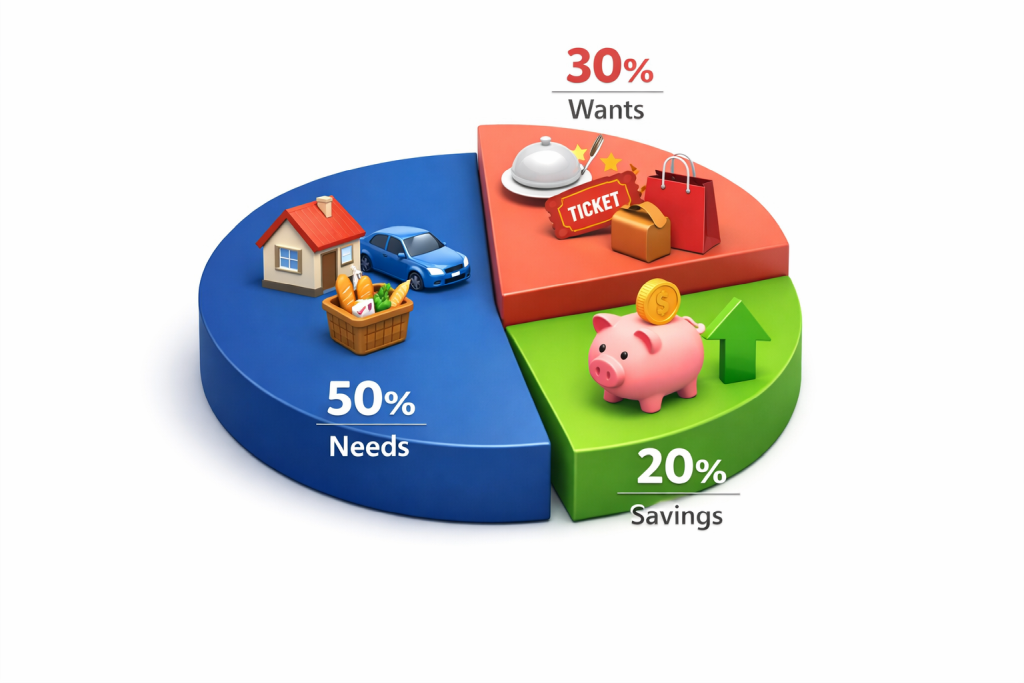

Step 3: Categorise Expenses Into Needs, Wants, and Savings

Now divide your spending into three buckets:

Needs (50-60%): Essential expenses you can’t avoid:

Housing (rent/mortgage, council tax)

Utilities (electricity, gas, water, internet)

Food (groceries only, not dining out)

Transport (car payment, insurance, fuel, or public transport)

Insurance (health, life, car, home)

Minimum debt payments

Wants (20-30%): Things you enjoy but could eliminate if necessary:

Dining out and takeaways

Entertainment (streaming, cinema, concerts)

Hobbies and recreation

Shopping (clothes, gadgets)

Gym membership

Subscriptions (Netflix, Spotify, etc.)

Savings & Debt Payoff (20%): Your future financial security:

Emergency fund (first priority)

Retirement contributions

Extra debt payments (beyond minimum)

Specific savings goals (house deposit, holiday, etc.)

Important: These percentages are guidelines, not rigid rules. If you live in London, your housing might be 40-50% alone. That’s fine, adjust the other categories accordingly.

Step 4: Choose Your Budgeting Method

Different methods work for different people. Choose based on your personality and financial situation.

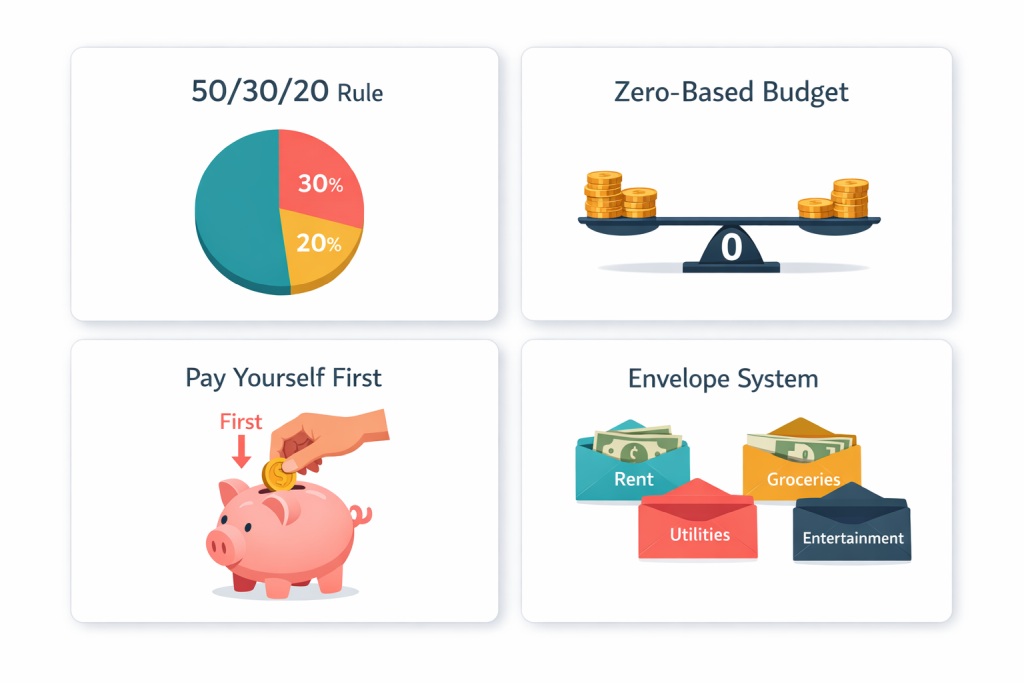

1. The 50/30/20 Rule (Best for Beginners)

50% needs, 30% wants, 20% savings. Simple, flexible, easy to remember.

Best for: People new to budgeting, moderate incomes, simple financial situations

Not ideal if: You have high debt, live in expensive city, or have irregular income.

2. Zero-Based Budget (Best for Debt Payoff)

Every pound gets assigned a job. Income minus expenses equals zero. Forces intentional spending.

Best for: Paying off debt aggressively, people who like detail, stable income

Not ideal if: You hate tracking, have variable income, or find it too restrictive

3. Pay Yourself First (Best for Savers)

Automatically save 10-20% when you get paid. Spend the rest guilt-free on needs and wants.

Best for: Building savings, people who hate tracking, good impulse control

Not ideal if: You have debt, overspend regularly, or live paycheque to paycheque

4. Envelope System (Best for Overspenders)

Allocate cash to different envelopes for each category. When the envelope is empty, you stop spending in that category. Digital versions available in apps.

Best for: Visual learners, overspenders, specific problem areas (like dining out)

Not ideal if: You prefer cards, find cash inconvenient, or have mostly fixed expenses

My recommendation: Start with 50/30/20. If that feels too loose, try zero-based. If it feels too restrictive, try pay yourself first. You can always switch methods.

Step 5: Cut Expenses (The Smart Way)

If your current spending exceeds your income, you need to cut expenses. But do it strategically—not through sheer willpower.

Easy wins (do these first):

- Cancel unused subscriptions (average household wastes £50/month)

- Switch insurance providers (save £200-400/year on average)

- Reduce energy usage (smart thermostat saves £150/year)

- Meal plan and grocery shop with a list (reduces food waste 30%)

- Use cashback and comparison sites for regular purchases

Medium wins (require some effort):

- Downgrade phone contract (switch to SIM-only saves £20-40/month)

- Reduce dining out frequency (cook 2 more meals weekly saves £120/month)

- Consolidate streaming services (rotate instead of keeping all)

- Shop own-brand groceries (saves 20-30% on food)

- Reduce car usage (walk/cycle short trips saves £50/month in fuel)

Big wins (lifestyle changes):

- Move to cheaper accommodation (biggest single expense for most)

- Sell expensive car, buy cheaper/use public transport

- Refinance high-interest debt

- Get a flatmate (cuts housing costs 30-50%)

For practical ways to save money quickly without drastically changing your lifestyle, check our comprehensive guide on saving strategies.

Important principle: Cut ruthlessly on things you don’t value, spend generously on things you do. A budget shouldn’t eliminate joy, it should fund what matters most to you.

Step 6: Build an Emergency Fund (Your Budget’s Safety Net)

The Federal Reserve reports that 37% of Americans would struggle to cover a £300 emergency expense, highlighting why emergency funds are critical.

Without an emergency fund, one unexpected expense destroys your budget and sends you into debt. This is your first savings priority.

Emergency fund targets:

Starter: £500-1,000 (covers most small emergencies)

Intermediate: One month’s essential expenses

Full: 3-6 months of expenses (6 months if self-employed or single income)

Build this before aggressively paying off debt (except high-interest credit cards). It prevents you from going deeper into debt when emergencies happen.

Where to keep it: High-yield savings account. Easy access, earns interest, separate from daily spending. Don’t invest emergency funds, you need guaranteed access.

Step 7: Tackle Debt Strategically

Once you have a starter emergency fund (£500-1,000), prioritise debt payoff. Debt is the biggest obstacle to financial freedom.

Two proven methods:

Debt Snowball (Better for motivation):

- List debts from smallest to largest balance Pay minimums on everything

- Throw all extra money at smallest debt

- When paid off, attack next smallest with combined payment

- Quick wins build momentum and motivation

Debt Avalanche (Better mathematically):

- List debts from highest to lowest interest rate

- Pay minimums on everything

- Attack highest interest debt first

- Saves most money on interest

- Requires more discipline (slower visible progress)

Paying off debt not only frees up money in your budget but can also improve your credit score – learn proven strategies in our 90-day credit improvement guide.

Priority order for extra payments:

- Payday loans/high-interest debt (20%+ interest)

- Credit cards (15-25% interest)

- Personal loans (8-15% interest)

- Car loans (5-10% interest)

- Student loans (3-7% interest)

- Mortgage (2-5% interest – usually pay minimum while investing)

Step 8: Automate Everything Possible

The secret to budget success isn’t willpower—it’s automation. Remove decisions from the equation.

Automate these on payday:

- Savings transfer to separate account (pay yourself first)

- Emergency fund contribution (until fully funded)

- Debt payments (beyond minimums)

- Fixed bills (rent, utilities, insurance, subscriptions)

- Retirement contributions (workplace pension or ISA)

After automation, what’s left in your current account is truly available to spend. This eliminates the mental math of “Can I afford this?”

Recommended account structure:

- Primary current account: Receives income, pays automated bills

- Spending account: Gets weekly/monthly transfer for variable expenses

- Savings account: Emergency fund and short-term goals

- Investment account: Long-term retirement and wealth building

Step 9: Review and Adjust Monthly

Your budget isn’t set in stone. Life changes. Expenses change. Review monthly and adjust.

Monthly budget review (10 minutes):

- Compare actual spending to budget

- Identify categories where you overspent

- Adjust next month’s budget if needed (was overspending a one-off or pattern?)

- Celebrate wins (stayed under budget, paid off debt, hit savings goal)

- Update for upcoming irregular expenses (Christmas, car service, insurance renewal)

Quarterly budget review (30 minutes):

- Reassess financial goals (still relevant?)

- Check emergency fund progress

- Review subscriptions (still using? better deal available?)

- Consider income increases (time for raise? side income opportunities?)

- Audit major expenses (insurance renewal coming? better mortgage rate available?)

Don’t treat budget violations as failures. They’re data. Use them to build a more realistic budget.

Step 10: Handle Irregular Income

Freelancers, commission earners, and seasonal workers face unique budgeting challenges. Traditional budgeting assumes steady income, you need a different approach.

The buffer method:

- Calculate your minimum monthly expenses (everything in ‘needs’ plus essential wants)

- Save one month’s expenses as a buffer (separate from emergency fund)

- Pay yourself a ‘salary’ from the buffer each month

- When income arrives, replenish the buffer first

- Anything above buffer goes to savings, debt, or discretionary spending

Example: Your essential monthly expenses are £2,000. Build a £2,000 buffer. Every month, transfer £2,000 from buffer to checking. When you earn £3,500, put £2,000 back in buffer, £1,500 towards savings/debt/extras.

Alternative: Budget on lowest income:

- Look at last 12 months of income

- Find your lowest earning month

- Budget as if you earn that amount every month

- Anything above goes to savings or debt

- Very conservative but eliminates stress

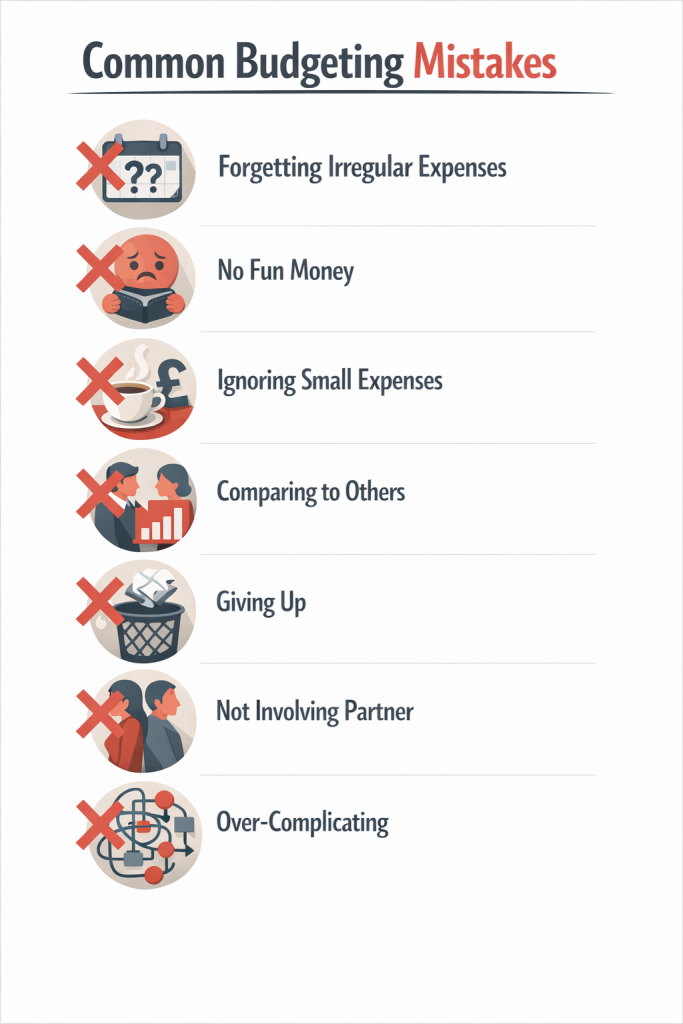

Common Budget Mistakes to Avoid

Forgetting irregular expenses: Car insurance, Christmas, birthdays, and annual subscriptions aren’t ‘unexpected.’ Divide annual costs by 12 and budget monthly.

No fun money: Budgets without discretionary spending fail. Even £50/month for guilt-free spending prevents resentment and burnout.

Ignoring small expenses: £3 daily coffee = £90/month. Small expenses add up. Don’t ignore them.

Comparing to others: Someone else’s budget percentages don’t matter. Your budget should reflect your income, location, and goals.

Giving up after one bad month: You will overspend sometimes. That doesn’t mean your budget failed, adjust and continue.

Not involving your partner: If you share finances, budgets require teamwork. Have monthly budget meetings together.

Over-complicating: Tracking 50 categories sounds organized but becomes impossible. Keep it simple, 10 categories maximum.

Frequently Asked Questions

How much should I budget for groceries?

Average UK household spends £40-60 per person per week on groceries. Single person: £160-240/month. Couple: £320-480/month. Family of four: £640-960/month. These are guidelines, adjust based on your dietary needs, location, and cooking habits. Meal planning and shopping with a list can reduce this by 20-30%.

What if my income doesn’t cover my expenses?

You have two options: cut expenses or increase income. Start with expense cuts (they’re faster). Cancel non-essentials, reduce variable spending, shop cheaper alternatives. If you’ve cut to the bone, focus on income, ask for a raise, take overtime, start a side hustle, or consider career change. Living beyond your means isn’t sustainable.

How often should I check my budget?

Weekly quick check (5 minutes): Ensure you’re on track with variable spending. Monthly review (10 minutes): Compare actual to budget, adjust categories if needed. Quarterly deep dive (30 minutes): Reassess goals, audit subscriptions, review major expenses. Don’t obsess daily, that’s exhausting and unnecessary.

Should I include my partner’s income in the budget?

If married or in long-term partnership with shared expenses, yes, budget together with combined income. If dating or keeping finances separate, each person maintains their own budget for personal expenses, but create a third budget for shared costs (rent, utilities, groceries) funded proportionally to income. Communication is key.

What’s the best budgeting app?

YNAB (You Need A Budget) is excellent for zero-based budgeting. Mint is free and automatic. Emma and Money Dashboard are great UK options. Goodbudget does digital envelope budgeting. Honestly? A simple spreadsheet works just as well. The best tool is the one you’ll actually use. Start simple, upgrade if needed.

How do I budget for Christmas without going into debt?

In January, estimate total Christmas spending (gifts, food, decorations, travel). Divide by 11 months. Save that amount monthly in separate account. If you typically spend £1,100 at Christmas, save £100/month starting February. When December arrives, you have cash ready. No debt, no stress, no January regret.

Can I budget if I’m paid weekly?

Absolutely. Either budget by week (divide monthly expenses by 4.3) or use the ‘buffer method.’ Save one month’s expenses. Pay all bills monthly from buffer. Replenish buffer with weekly wages. This smooths weekly income into monthly payments. Most bills are monthly anyway, so this prevents the ‘five paycheck month’ confusion.

Conclusion

You now have everything you need to create a budget that actually works. Not a restrictive punishment that you’ll abandon in three weeks, but a flexible framework that helps you control your money without controlling your life.

Start simple. Pick a budgeting method, track expenses for a month, adjust as needed. Automate what you can, review monthly, and be patient with yourself. Financial habits take time to build.

Remember: the goal isn’t perfection. The goal is progress. A budget that you stick with 80% of the time is infinitely better than a ‘perfect’ budget you abandon after two weeks.

Your future self, the one with an emergency fund, shrinking debt, and actual savings, will thank you for starting today.