How to Improve Your Credit Score in 90 Days: Proven Guide

You’ve just been rejected for a mortgage. Or that car loan came back with an eye-watering interest rate. Or you simply checked your credit score and discovered it’s shockingly low. Now you need to fix it, fast.

Good news: improving your credit score isn’t a years-long process. With focused effort and the right strategies, you can learn how to improve your credit score and see significant improvement in 90 days. People regularly increase scores by 50-100 points in three months.

Experian explains that UK credit scores range from 0-999, with scores above 700 considered good and 900+ excellent. Whether you’re starting from 450 or 650, this 90-day plan gives you actionable steps to boost your score quickly.

This guide covers exactly what impacts your credit score, common mistakes destroying it, and a week-by-week action plan. No gimmicks, no “magic fixes”, just proven strategies that actually work.

Let’s rebuild your credit.

Understanding What Affects Your Credit Score

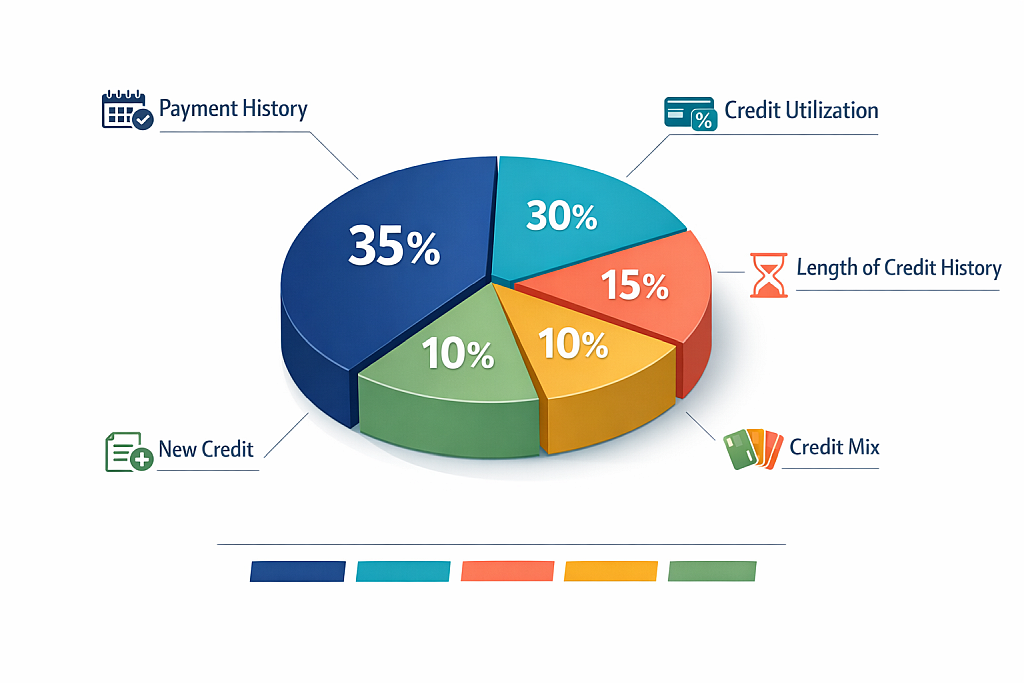

Before improving your score, understand what creates it. UK credit agencies (Experian, Equifax, TransUnion) evaluate these factors:

Payment History (35% of score):

Most important factor

- Tracks whether you pay bills on time

- Late payments (30+ days) stay on report for 6 years

- Recent missed payments hurt more than old ones

- County Court Judgements (CCJs) and defaults are severe

Credit Utilization (30% of score):

Percentage of available credit you’re using

- Under 30% is good, under 10% is excellent

- Example: £3,000 limit, £900 balance = 30% utilization

- Calculated per card AND across all cards

- Maxed-out cards severely damage score

Length of Credit History (15% of score):

- Average age of all credit accounts

- Older accounts = better score

- Closing old accounts shortens history

- This factor improves slowly (can’t be rushed)

Credit Mix (10% of score):

- Variety of credit types (credit cards, loans, mortgage)

- Managing different types responsibly shows competence

- Don’t open accounts just for this—minor factor

New Credit (10% of score):

- Recent credit applications and inquiries

- Multiple applications in short time = red flag (“credit hungry”)

- Hard inquiries stay on report 12 months

- Soft checks (checking your own score) don’t affect score

Key insight: Payment history and credit utilization make up 65% of your score. Focus there for fastest improvement

Week 1-2: Foundation and Error Correction

Days 1-3: Get Your Credit Reports

Citizens Advice recommends checking your credit report from all three main agencies: Experian, Equifax, and TransUnion, since they may hold different information.

Where to check (all free):

- Experian: ClearScore app (updates monthly)

- Equifax: ClearScore also provides this

- TransUnion: Credit Karma app (updates weekly)

- Statutory reports: Request from each agency directly (£2 each or free if digital)

What you’re looking for:

- Errors (wrong addresses, accounts you didn’t open, incorrect balances)

- Fraudulent accounts

- Outdated information (old addresses still listed)

- Accounts showing as open that you’ve closed

- Incorrect payment history

Important: Studies show 1 in 4 credit reports contain errors. Finding and fixing these can boost your score 20-50 points immediately.

Days 4-7: Dispute Any Errors

Found errors? Dispute them immediately. Agencies must investigate within 28 days.

How to dispute:

- Use online dispute forms (fastest) on each agency’s website

- Provide specific details: account number, error description, correct information

- Upload proof if you have it (statements, payment confirmations)

- Keep copies of all correspondence

- Follow up if no response within 28 days

Common successful disputes:

- Duplicate accounts (same debt listed twice)

- Payments marked late that were actually on time

- Accounts belonging to someone else (similar name/address)

- Settled debts still showing as active

- Information older than 6 years (should be removed)

Days 8-14: Register on Electoral Roll

Not on the electoral roll? This single action can add 50+ points to your score.

Why it matters:

- Verifies your name and address

- Proves residency stability

- Required by most lenders for credit applications

- Free and takes 5 minutes online

How to register:

- Go to gov.uk/register-to-vote

- Provide name, address, National Insurance number

- Takes effect within days

- Updates automatically appear on credit reports within 4-6 weeks

Privacy option: You can register but opt out of the public register (prevents marketing companies accessing your info). Still helps your credit score.

Week 3-4: Reduce Credit Utilization Aggressively

This is where you’ll see the biggest score jump. Credit utilization is the fastest factor to improve.

The goal: Get under 30%, ideally under 10%

Strategy 1: Pay Down Balances

Before you can consistently pay down credit card balances, you need to create a realistic budget that prevents new debt while freeing up money for payments.

Attack plan:

- List all credit card balances and limits

- Calculate current utilization (balance ÷ limit × 100)

- Pay down cards over 30% first (biggest impact)

- If limited funds, spread payments to get ALL cards under 50%, then under 30%

- Make payments before statement date (not just due date) for faster reporting

- If you’re struggling to find money for extra credit card payments, our guide covers practical ways to save money quickly without drastically changing your lifestyle.

Example:

- Card A: £900/£1,000 limit = 90% (PAY THIS FIRST)

- Card B: £1,500/£3,000 limit = 50%

- Card C: £400/£2,000 limit = 20% (already good)

- With £600 to pay: Put £500 on Card A (drops to 40%), £100 on Card B (drops to 47%). Next month, finish Card A, then tackle Card B.

Strategy 2: Request Credit Limit Increases

Increasing your limit without increasing balances instantly improves utilization.

When to request:

- Account open 6+ months

- No late payments in past year

- Your income has increased

- You’ve been a responsible customer

How to request:

- Call card issuer or use online request form

- Ask for specific increase (e.g., from £2,000 to £4,000)

- Some do soft credit check (doesn’t hurt score), others do hard check (slight temporary dip)

- If approved, don’t spend more—keep balance same, utilization drops

Example impact:

- £1,500 balance on £3,000 limit = 50% utilization

- Limit increases to £6,000

- Same £1,500 balance = 25% utilization

- Score improves without paying a penny

Strategy 3: Make Multiple Small Payments

Instead of one large payment per month, make weekly payments. Keeps reported balance lower.

Why this works:

Credit cards report balance to agencies on statement date (not due date)

Paying throughout month keeps balance low when reporting happens

Example: £1,000 spending/month, £3,000 limit. Pay £250 weekly instead of £1,000 monthly. Statement shows £250-500 instead of £1,000

Week 5-6: Perfect Your Payment History

Payment history is 35% of your score. One missed payment can drop your score 50-100 points.

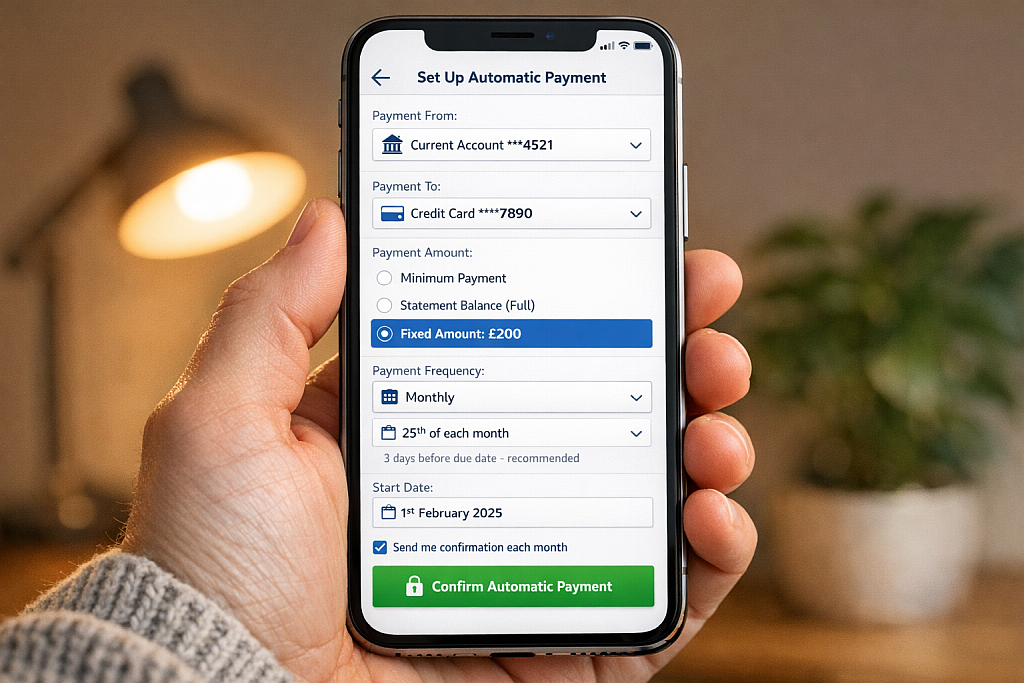

Set Up Automatic Payments

Never miss a payment again. Automate everything.

What to automate:

- Credit card minimum payments (set up through card issuer)

- Loan payments (car, personal, student)

- Mortgage/rent if possible

- Utility bills (water, electric, gas)

- Phone contract

Strategy:

- Automate minimum payments to guarantee on-time

- Make manual additional payments when you can

- Set calendar reminder 5 days before due date to check automation worked

- Keep buffer in account to prevent bounced payments

- Goodwill Letter for Past Late Payments

- If you have one or two late payments and have been perfect since, try asking creditor to remove them.

Template:

“Dear [Creditor],

I’m writing to request removal of the late payment reported on [date]. I’ve been a customer for [X] years and this was an isolated incident due to [genuine reason, job loss, medical emergency, oversight]. Since then, I’ve made all payments on time for [X] months. I would greatly appreciate your consideration in removing this mark. I value our relationship and intend to continue as a responsible customer.”

Success rate: 30-50% if you have legitimate excuse and recent good history. Worth trying, no downside.

Week 7-8: Strategic Account Management

Don’t Close Old Accounts

This is counterintuitive but critical: closing old credit cards usually hurts your score.

Why keep them open:

- Reduces average credit age (15% of score)

- Decreases total available credit (worsens utilization)

- Removes positive payment history

What to do instead:

Keep old cards open, even if you don’t use them

- Make a small purchase every 3-6 months to prevent closure (£5 petrol, then pay off immediately)

- Cut up card if tempted to overspend, but don’t close account

- If annual fee, negotiate waiver or downgrade to no-fee version

Exception: Close the account if it has high annual fee you can’t waive and you have other old accounts maintaining your average age.

Become an Authorized User

If family member has excellent credit, ask to be added as authorized user on their card.

How it works:

- Their account’s positive history appears on your credit report

- You inherit the age of that account (helps length of history)

- You don’t need to use the card or even have physical card

- Can boost your score 20-60 points if added to old, well-managed account

Requirements:

- Primary cardholder must have excellent payment history

- Low credit utilization on that card

- Account at least 2+ years old (older is better)

- You trust them not to miss payments (their negatives affect you too)

Week 9-12: Build and Maintain Momentum

Continue Perfect Payment History

Every month of on-time payments strengthens your score. Payment history compounds over time.

Timeline:

- 3 months perfect payments: Recent negatives start fading in importance

- 6 months perfect payments: Noticeable score improvement

- 12 months perfect payments: Old late payments matter much less

- 24 months perfect payments: Excellent payment history established

Keep Utilization Low

Don’t undo progress. Maintain under 30% utilization permanently.

Ongoing habits:

Pay balance in full monthly if possible

If carrying balance, keep under 30% limit

- Spread large purchases across multiple cards to avoid maxing one

- Make payments before statement date for lower reported balance

- Avoid New Credit Applications

- During these 90 days, don’t apply for new credit unless absolutely necessary. Each hard inquiry drops score 5-10 points temporarily.

Exceptions where you can apply:

- Car loan when you need transport (but get quotes within 14-day window—counts as single inquiry)

- Mortgage pre-approval if seriously house hunting

- Refinancing high-interest debt to save significant money

What to avoid:

- Store credit cards (“Save 15% today!”)

- New credit cards just for rewards

- Financing purchases you could save for

- Multiple applications in short period

- Monitor Your Progress

- Check score monthly to track improvement and catch issues early.

What to watch:

- Score trend (should be climbing steadily)

- Credit utilization percentage

- New accounts or inquiries you didn’t authorize (fraud)

- Payment history (ensure all showing as on-time)

- Errors that may appear

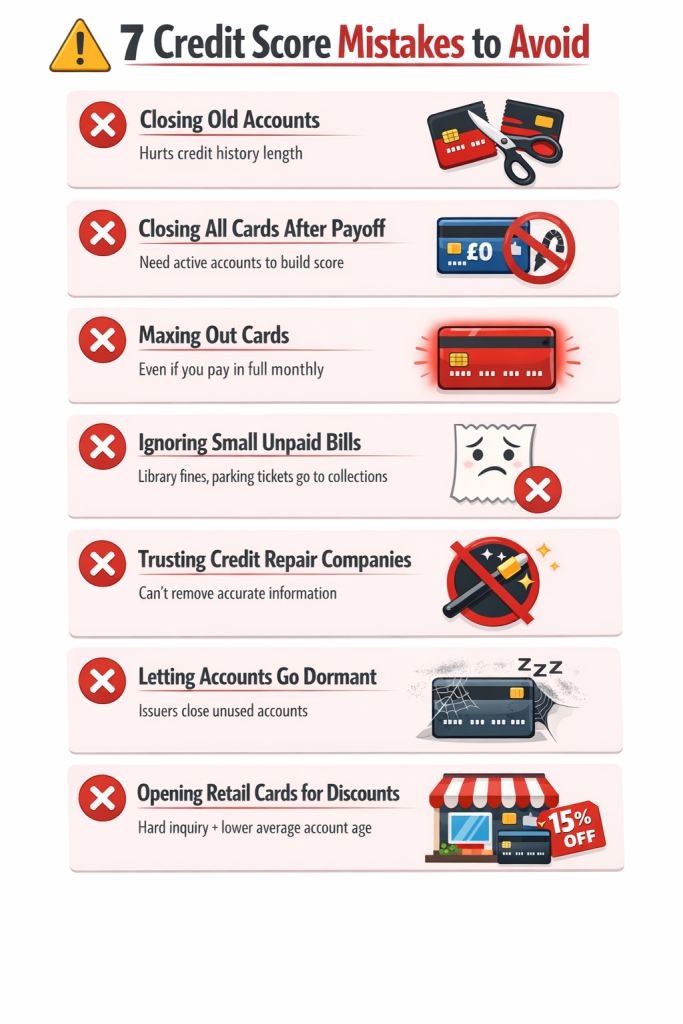

What NOT to Do (Common Mistakes)

Closing old accounts:

Hurts average age and utilization. Keep them open.

Paying off all debt and closing all credit cards:

Zero debt is good, but you need active credit accounts to build score. Keep 1-2 cards open with small balances paid monthly.

Maxing out cards even if you pay in full:

Utilization is calculated at statement date, not due date. High reported balance hurts even if you pay it off.

Ignoring small bills:

Unpaid library fines, parking tickets, medical bills can go to collections and devastate score. Pay or negotiate settlement.

Believing credit repair company promises:

No company can legally remove accurate negative information. They can only dispute errors, which you can do yourself for free.

Letting accounts go dormant:

Card issuers close unused accounts after 12-18 months. Use each card quarterly to keep active.

Opening retail credit cards for discounts:

That 15% saving costs you hard inquiry and lowers average account age. Not worth it.

Frequently Asked Questions

Can I really improve my credit score in 90 days?

Yes, if you take focused action. Disputing errors can add 20-50 points immediately. Reducing utilization from 80% to 30% can add 50-100 points. Three months of perfect payments starts rebuilding payment history. Typical improvement: 40-120 points depending on starting position and how aggressively you implement strategies.

What’s the fastest way to improve my score?

The one-two punch: (1) Dispute any errors on credit report (can boost 20-50 points within 28 days), (2) Pay down credit card balances to get utilization under 30% (can boost 50-100 points within one statement cycle). These two actions alone can add 70-150 points within 4-6 weeks.

Will checking my own credit score hurt it?

No. When you check your own score, it’s a “soft inquiry” and has zero impact. Only “hard inquiries” from lenders affect score (and only by 5-10 points temporarily). Check your score as often as you want, weekly monitoring is actually beneficial for catching errors and fraud early.

Should I pay collections accounts to improve my score?

Complicated answer. Paying collections won’t immediately improve score—the negative mark stays for 6 years from default date whether paid or not. However: (1) Some lenders won’t approve you with unpaid collections, (2) You can negotiate “pay for delete” (they remove it if you pay), (3) Newer scoring models weight paid collections less than unpaid. If seeking mortgage/car loan soon, pay them. If just building score, focus elsewhere first.

How long do negative items stay on my credit report?

Most negative marks stay 6 years from date of default: late payments, defaults, CCJs, debt management plans, IVAs. Bankruptcy stays 6 years. Hard inquiries stay 12 months but only affect score for a few months. The good news: impact fades over time. A 3-year-old late payment hurts much less than a 3-month-old one.

Is it better to pay off credit cards or save money?

Strategy: (1) Save £500-1,000 emergency fund first (prevents going deeper into debt when emergencies hit), (2) Attack high-interest credit card debt aggressively (anything 15%+ interest), (3) Build emergency fund to 3 months expenses, (4) Pay extra on remaining debt while also saving. Don’t choose between them after initial emergency fund, do both simultaneously.

Will getting a new credit card help or hurt my score?

Short term: Small drop (5-10 points) from hard inquiry and lower average account age. Long term (6+ months): Can help by increasing total available credit (better utilization) and building positive payment history. Only get new card if: (1) You pay existing cards in full monthly, (2) You need better rewards/rates, (3) You’re not applying for mortgage/car loan within 6 months.

Conclusion

Improving your credit score in 90 days isn’t magic, it’s methodical action. Dispute errors, reduce credit utilization, perfect your payment history, and maintain existing accounts. These four pillars drive 80% of score improvement.

Your week-by-week action plan: Get reports and dispute errors (weeks 1-2), aggressively reduce utilization (weeks 3-4), perfect payment automation (weeks 5-6), optimize account management (weeks 7-8), and maintain momentum (weeks 9-12).

Realistic expectations: Starting from 450? You can reach 550-600. Starting from 650? You can reach 700-750. The lower your starting point, the faster the initial gains. Progress slows as you approach excellent credit, but consistency compounds.

Remember: credit score improvement continues beyond 90 days. The habits you build now, automated payments, low utilization, regular monitoring, create lifelong financial benefits. Every month of responsible credit use strengthens your position.

Start today. Check your reports, set up automation, and begin the 90-day transformation. Your improved credit score opens doors to better interest rates, approved applications, and financial opportunities. You’ve got this.